Hong Kong banking system is characterized by a three-tier system, including Licensed banks, Restricted banks, and Deposit-taking companies. In this blog, we will delve into key features of each type!

1. A glance at the banking system in Hong Kong

The banking sector is of vital significance in the economic development of Hong Kong.

Not only has Hong Kong become flourishing in terms of offshore banking, but also a strong linkage between Hong Kong and offshore renminbi business to Mainland China has attracted much attention from most foreign investors in recent years.

Hong Kong is deemed a globally well-reputed financial hub. There are presences of more than 70 of the world’s 100 largest banks in Hong Kong. With the high concentration of international banks, Hong Kong is listed in the top ten biggest international banking mecca when it comes to the volume of external transactions.

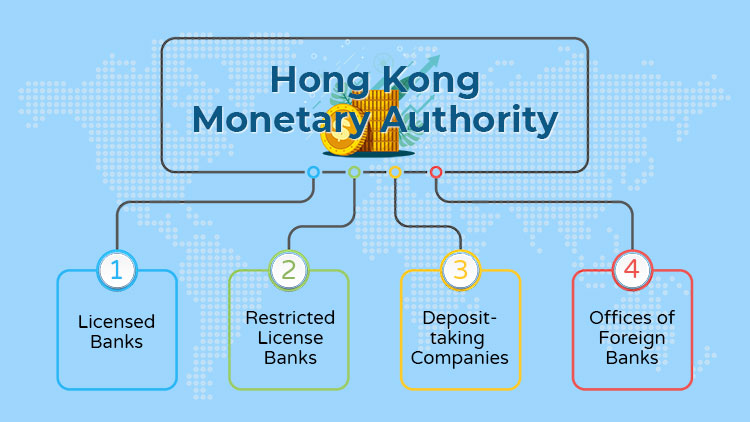

The banking system in Hong Kong is regulated under the Hong Kong Monetary Authority (HKMA). Except for the issuance of banknotes, most of the key duties of a central bank will be performed by HKMA. Hong Kong banking system is characterized by four main types of banks:

Licensed banks

Restricted license banks

Deposit-taking companies

Offices of foreign banks (Representative offices of overseas banks)

Other than representative offices, the banking system in Hong Kong is dominated by its three-tier system including three types of banking institutions as above. This system is categorized upon the amount of deposit, term of the deposit, and each one’s business nature. They are also collectively known as Authorized Institutions (AIs) supervised under the Banking Ordinance.

As per HKMA’s latest update to April 2020, the number of authorized institutions in Hong Kong was 193 in total, including 163 licensed banks, 17 restricted banks, and 13 deposit-taking companies in Hong Kong. Furthermore, the jurisdiction has 42 local representative offices of overseas banks, 8 locally incorporated companies in Hong Kong granted licenses for virtual bank operations, and 30 money broker approvals by the HKMA.

It should be noted that there are certain requirements as well as restrictions amongst three types. It is also interesting to know that only restricted banks and licenses banks – the first two forms – can be deemed as banks. In what follows, we will delve into key features of the three-tier banking system in Hong Kong.

Need an a-to-z guide to doing business in Hong Kong? This e-book provides you with the latest information about:

Incorporation process

Annual compliance requirement

Hong Kong tax system

Hiring issues for Hong Kong Business

2. Features of three-tier banking system in Hong Kong

The table below represents key highlights of three-tier banking system in Hong Kong:

Accept deposits of any size and maturity from the public

Accept deposits of any maturity of HK$500,000 and above

Accept deposits of HK$100,000 or above with an original term of maturity of at least three months

Minimum capital requirement of HK$300 million

HK$100 million

HK$25 million

Licensed Banks can be incorporated inside or outside Hong Kong.

Virtual banks are allowed in Hong Kong and categorized as licensed banks.

Restricted License Banks can be incorporated inside or outside Hong Kong.

All deposit-taking companies are incorporated in Hong Kong.

Licensed Banks

Only this type of bank may carry out “banking business” related activities as prescribed under the Banking Ordinance. These activities can be accepting deposits, providing retail customers current, checking, savings, or other similar accounts, granting loans, paying or collecting cheques drawn paid in by customers, etc. Licensed banks are allowed to accept any deposits regardless of size and maturity.

The minimum capital requirement (including paid-up share capital and balance of share premium account) for licensed banks is HK$300 million, which is much higher than that for the other two types of banks. It should be also noted that only licensed banks in Hong Kong must observe the minimum-size criteria which are required to hold HK$3 billion public deposits and have total assets of at least HK$4 billion.

Currently, Hong Kong has 31 domestically licensed banks and 132 licensed banks incorporated outside Hong Kong. Licensed banks in Hong Kong protect their depositors through the Deposit Protection Scheme with the allowable maximum protection of up to HK$500,000 per depositor.

Restricted Banks

Restricted license banks are actually merchant banks and investment banks. This type of bank is not allowed to carry out a range of banking business like the above-mentioned fully licensed banks. As its name denoted, there is a restriction for restricted banks. In terms of deposits, the bank only accepts deposits of no less than HK$500,000.

Another key to mention is that restricted banks in Hong Kong typically take deposits for short-term periods with either a period of notice or an original term to maturity of 3 months in maximum. In Hong Kong, a total of 17 restricted license banks, including 12 banks incorporated in Hong Kong are available.

Deposit-taking companies

These are companies established or connected with the licensed banks or banks incorporated outside Hong Kong. Deposit-taking companies are allowed to engage in consumer finance, commercial lending, and securities-related business activities.

Unlike the other two types of deposit-taking institutions, these companies may take deposits of HK$100,000 or above with an original term to maturity lasting more than 3 months.

Up to now, 13 deposit-taking companies in Hong Kong are all incorporated inside Hong Kong.

3. Banking system in Hong Kong & other related matters

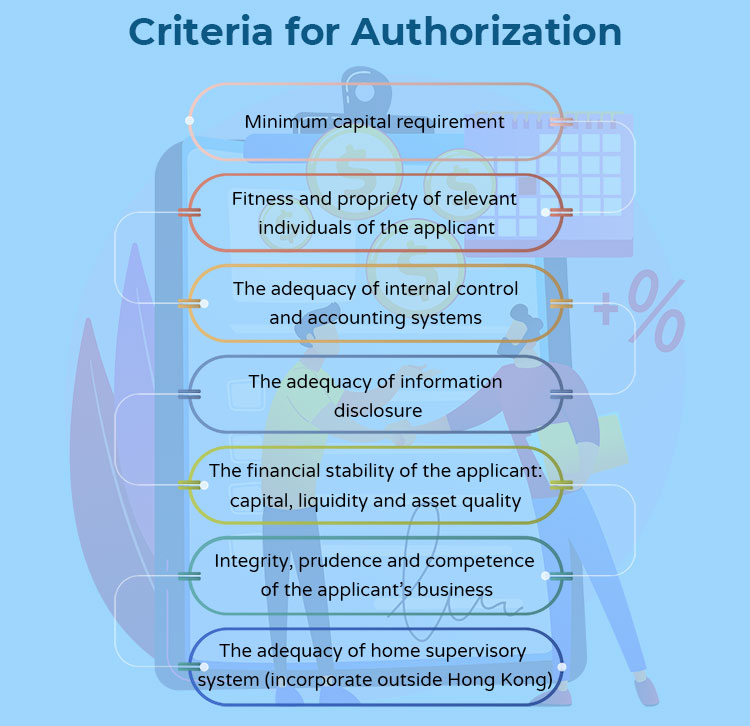

Criteria for authorization

All authorized institutions in Hong Kong are subject to the minimum criteria for authorization as prescribed in the Seventh Schedule to the Banking Ordinance. If any banking applicants do not satisfy one of these criteria, the HKMA may reject their application. Note that such conditions must be met and maintain both at the time of application being made and after authorization.

What are these minimum criteria? Below are the key criteria that applicants should bear in mind:

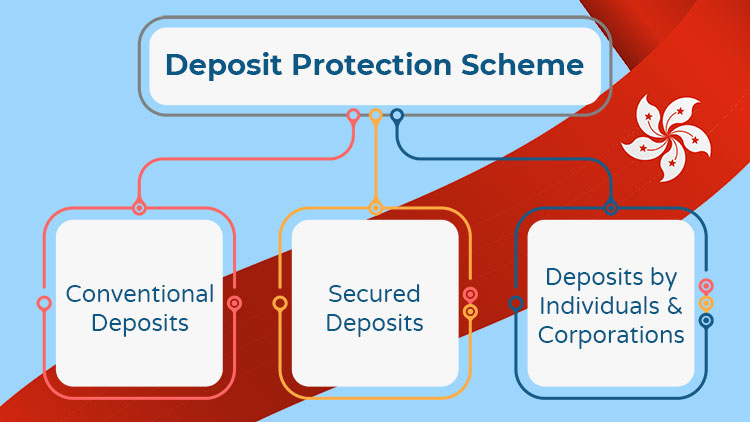

Deposit Protection Scheme

Deposit Protection Scheme (DPS) was launched in 2006 under the Deposit Protection Scheme Ordinance. This scheme is to protect deposits held by licensed banks in Hong Kong by giving them compensation in case of bank failure. Note that deposits, if eligible, will be put under the protection by the DPS automatically; therefore, they do not need to apply for compensation. Depositors covered under the DPS of Hong Kong, whether to be an individual or a company, can be compensated up to a max of HK$500,000.

Deposits qualifying with this scheme include conventional deposits like savings, current accounts, time deposits time with a term not exceeding 5 years, secured deposits, and any deposits by individuals and corporations, except for structured deposits, offshore deposits, or bearer instruments. Moreover, protected deposits can be in HK dollar, renminbi, or any kind of foreign currency.

Note, however, that deposits taken by restricted license banks and deposit-taking companies are not under the protection of this scheme.

Virtual banks

A virtual bank does not deliver its business activities in physical branches. It refers to the bank principally conducting retail banking services via the internet or some other means of electronic vehicles. The emergence of virtual banking in Hong Kong plays an important role in marking the footstep of Hong Kong into the Era of Smart Banking.

Below is a summary of key points regarding virtual bank requirements in Hong Kong:

Virtual banks are subject to a set of supervisory obligations as same as the conventional banks in Hong Kong, including the minimum requirement for authorization under the Seventh Schedule of the Banking Ordinance.

Virtual banks in Hong Kong shall not impose any minimum account balance requirement/low-balance fees on the bank’s customers.

Virtual banks should be formed as locally incorporated banks. Maintaining a physical presence is a must for any virtual bank applicant in Hong Kong.

Virtual banks are required to maintain adequate capital which must be well-matched with their operations and banking risks. Term and conditions upon the benefits and obligations of the bank and customers must also be clearly set out from the bank’s commencement.

To get a virtual bank licensed in Hong Kong, there are some important documents submitted on the application, some of which include a credible and viable business plan, an exit plan, an assessment report of its technology system, a description of risk-based management, etc.

*NOTE: You should not misunderstand the concept of Virtual Banks with fintech platforms, aka Money Service Operators (MSOs) in Hong Kong. A big plus for these fintech solutions is that you do not need to visit Hong Kong for opening a bank account. The presences of MSOs increasingly become widely-used alternatives to traditional banks and virtual banks in Hong Kong.

While BBCIncorp strives to make the information on this website as timely and accurate as possible, the information itself is for reference purposes only. BBCIncorp would like to inform readers that we make no representation or warranty, express or implied. Feel free to contact BCCIncorp’s customer services for advice on specific cases.