Economic substance legislation has been introduced on many offshore jurisdictions worldwide as a signal for responding to EU and OECD initiatives in curbing harmful tax approaches. A prestigious financial offshore center like BVI does not lie outside such implementation.

In this article, BBCIncorp offers you a comprehensive guide to BVI Economic Substance Requirements that you should know.

You may want to try our online test below:

1. Overview of BVI Economic Substance Act (BVI ESA)

Economic Substance is the center of attention to any “no or only nominal tax” offshore jurisdiction, including the British Virgin Islands.

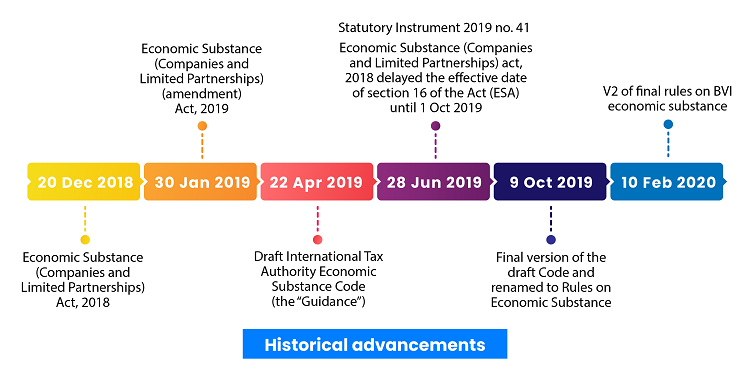

In reaction to commitment for adherence to the EU listing process and OECD BEPS Inclusive Framework, BVI has issued the Economic Substance (Companies and Limited Partnerships) Act, 2018. The regime officially came into force on 1st January 2019.

On 30 January 2019, some amendments were ratified to the Act (the “Economic Substance Act”).

On 22 April 2019, the draft International Tax Authority Economic Substance Code (the “Guidance”) was introduced with several supplements to the previous version of the Economic Substance Act.

The Economic Substance (Companies and Limited Partnerships) (Amendment) Act 2021 has officially come into force on 29 June 2021. This is after some amendments were made to the Economic Substance (Companies and Limited Partnerships) Act, 2018 (ESA).

The key points are related to the limited partnerships without legal personality and clarification that “investment fund business” is not considered a relevant activity.

(1) Limited partnership

The update ensures that all BVI limited partnerships (with or without legal personality) are now considered to be a “legal entity”. Therefore, they now fall within the scope of Economic Substance Regulations.

All registered BVI limited partnerships are subject to the compliance requirements and reporting obligations of the BVI Economic Substance.

(2) Investment Fund Business

The BVI Economic Substance Amendment Act 2021 adds definitions of “investment fund” and expressly excludes Investment Fund Business from being a relevant activity within the scope of BVI ES Regulations.

The final Code on BVI economic substance as the renamed Rules (and Explanatory Notes) on Economic Substance (the Rules) was released by the International Tax Authority (the ITA) on 9 October 2019. The updated version of the final rule was then published in February 2020.

It specified some adjustments set out by the Code of Conduct Group, as well as clarified further details regarding the reporting requirement and submission period under the BVI ESA.

You can find the original version of the final rules here.

The law sets out economic substance requirements and reporting for BVI legal entities that are not tax-residents in other jurisdictions and carry on relevant activities.

Pursuant to the Amendment Act 2021, the “legal entity” concept encompasses all registered BVI companies and limited partnerships (with or without a separate legal personality).

On the other side, an entity is considered to be out-of-scope of the ‘legal entity’ definition if it is a non-resident company that is a tax resident in the country other than BVI.

In terms of “relevant activity”, in the context of the economic substance regime, the OECD and EU demonstrate nine geographically mobile “relevant activities” which cover various ranges of business sectors. They include:

- Banking

- Insurance

- Fund management

- Finance and leasing

- Headquarters

- Shipping

- Holding company

- Intellectual property

- Distribution and service centers

As regulated by the final rule on this law, when a legal entity carries on a relevant activity, that entity must be subject to the economic substance requirements and reporting submission in respect to that relevant activity.

In what follows, we will delve into what BVI companies need to do to comply with the BVI economic substance regime!

3. Compliance duties and reporting obligation

3.1. Compliance duties under BVI ES

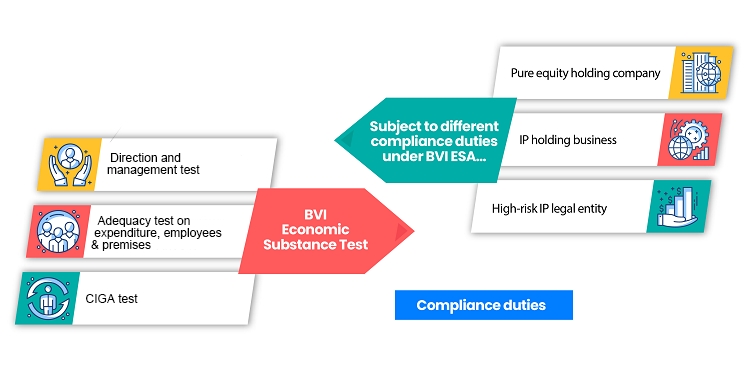

Under the BVI Economic Substance Act, all BVI companies and limited partnerships, including BVI business companies with legal personality engaging in one or more relevant activities must fulfill the compliance duties (economic substance test) for each relevant activity to be involved.

Be advised that depending on your type of business entity and business category, the requirements can also vary.

For legal entities that carry on relevant activities (except for pure equity holding entities)

Legal entities (pure equity holding entities excluded) can satisfy the economic substance test in the BVI if the three conditions below are met:

- Direction and management test: The entity must guarantee its relevant activities to be directed and controlled inside the territory of BVI during its financial period.

- “Adequacy” test on expenditure, number of employees, premises, and equipment located in BVI: In particular, the entity must guarantee:

– Having an adequate number of qualified employees to conduct the relevant activity in the BVI;

– Incurring the sufficient operational expenses for the relevant activity in the BVI;

– Having an appropriate physical presence for conducting its core income-generating activities;

– In case the entity is engaging in IP business in which specific equipment will be used, that equipment must be situated within the BVI.

- CIGA test: The entity must conduct certain Core Income-Generating Activities (CIGA) in the BVI. Core income-generating activities are defined under section 7 of the Act and vary according to types of businesses.

The given table shows some typical CIGAs in relation to the nine relevant activities under BVI ESA.

| Relevant activities | Core Income Generating Activities |

| Banking business | Raising funds, managing credit or currency risks, providing loans and credit, managing regulatory capital, etc. |

| Insurance business | Predicting and calculating risk, insuring or re-insuring against risk, providing business services on insurance. |

| Fund management business | Making decisions on holding and sales of investments, calculating risks and reserves, taking decisions on currency, etc. |

| Finance and leasing business | Agreeing on funding terms, identifying and acquiring leased assets, revising related agreements, etc. |

| Headquarters business | Making management decisions, incurring costs on behalf of affiliates, coordinating group activities. |

| Shipping business | Hiring and managing crew members, hauling and maintaining ships, scheduling voyages, etc. |

| Intellectual property business | Concerning intellectual property assets (patents, R&D) or non-trade intangible assets (brand, trademark and customer data, branding and distribution). |

| Distribution and service center business | Transporting and storing items, managing stocks, taking orders, providing consulting solutions |

For the pure equity holding company

Section 8 (2) defined a pure equity holding company in the British Virgin Islands as the entity that “carries on no relevant activity other than holding equity participations in other entities and earning dividends and capital gains”.

It should be noted that if you register a pure equity holding entity only holding equity participation in other entities through which you earn dividends and capital gains, then your entity can be entitled to a less complicated compliance duty to satisfy the economic substance requirement.

Particularly, the pure equity holding company is to have its economic substance if it complies with the following requirements:

- It complies with relevant regulations under which it is governed – i.e. BVI Business Companies Act, 2004 or the Limited Partnership Act, 2017; and

- It has adequate premises and employees in BVI for passively holding or actively managing the equity participation.

For intellectual property (IP) holding business

This type of entity is presumed to not conduct core income-generating activity if activities carried on within BVI don’t include activities specified in section 7 of the Act. To rebut the presumption, the entity must prove that its activities within BVI include:

- Strategic decisions and management of the principal risks pertaining to the development and exploitation of intangible assets;

- Strategic decisions and management of the principal risks pertaining to acquisition by third parties and exploitation of intangible assets;

- Underlying trading activities of intangible asset exploitation and income generation from third parties.

As for high-risk IP legal entities, the presumption can be contested if it can show the activities of development, exploitation, maintenance, enhancement, and protection of intangible assets are performed by its suitably qualified employees who are on long-term contracts and physically present in the BVI.

3.2. Reporting obligations

Legal entities are required to fulfill reporting obligations on their activities yearly. Importantly, such reports must be processed via their registered agent located in the British Virgin Island. And documents required for your report may vary according to your business category and tax residency status.

To make it clear, we put into classifications below groups of reporting information:

| Entity | Required documents | Submission Date |

| Legal entities being BVI tax residents and conducting relevant activities | -Total revenue earned by the relevant activity in BVI; -The entire operation spending on and by the relevant activity in BVI; -The sum of qualified employees engaging in relevant activity in BVI; -Address of premises in BVI in relation to the relevant activity; -Details of equipment in BVI in relation to the relevant activity; -Specifics of individuals in charge of direction and management of the relevant activity, and whether they are resident in BVI; -Information on the outsourcing entity and deployed resources (if CIGAs are outsourced to another company). | Within 6 months of the end of their financial period (or 18 months from the commencement of the financial period from 30 June 2019) * *Further details on the reporting timeline are mentioned in Part 4 of this article |

| IP holding business | -Above-mentioned information is required; -Whether they are high-risk IP business; -Whether they want to contest the rebuttable presumption as prescribed in the Act (plus related documents) |

| Legal entities conducting relevant activities, and NOT tax residents in BVI | - Details and support evidence regarding your tax residency country

|

Note: Legal entities NOT engaging in any relevant activity regulated under BVI ESA must deliver a notification to their registered agent in BVI. The good news is that there is no need to provide further supporting evidence in this case.

Exchange of information is processed by the connection between the BVI and the competent tax authority in which your company is a tax resident.

If your company is proven to be a non-tax resident in the BVI then the relevant authority which is the ITA will then notify the overseas competent tax authority located in the foreign jurisdiction.

As for the case in which your company has one beneficial owner being an EU member state, the ITA will also deliver a notification on the tax residency claim of your company to the corresponding authority in that EU member state.

In addition, exchanging economic substance details can also be conducted by the ITA to the overseas tax authority of one non-resident entity in BVI if that entity falls into the following circumstances:

- The entity has violated the economic substance rules in BVI; or

- The entity engages in IP business and falls in the presumption of not carrying out CICA within BVI.

4. Compliance timeline

The ESA regulated that a legal entity must comply with economic substance requirements for any financial period in which it carried out relevant activities.

The financial period of the legal entity can be determined as the following cases:

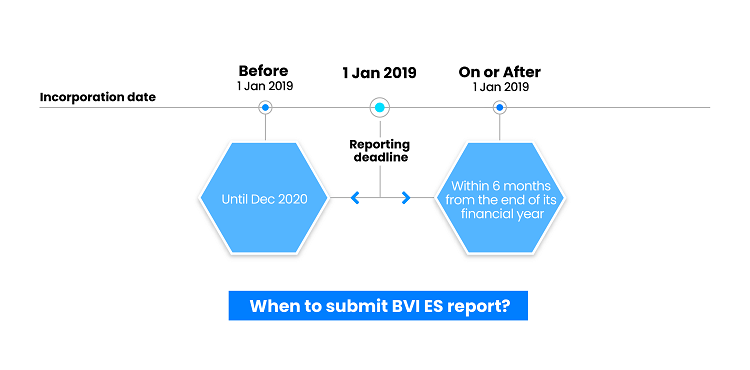

- For companies and limited partnerships (with legal personality) incorporated on or after 1 Jan 2019, the financial period is within 1 year from the date of incorporation.

- For companies and limited partnerships (with legal personality) incorporated before that date, the financial period will rest for one year and start no later than 30 Jun 2019. In other words, such entities don’t have to comply with substance regulation until 30 Jun 2019.

Regardless of engaging in relevant activities or not, all legal entities must submit an annual economic substance report within 6 months from the end of their financial year.

The financial period of the BVI limited partnerships without legal personality has been updated as the following:

For BVI limited partnerships without legal personality formed before 1 July 2021, their first “financial period” must commence no later than 1 January 2022.

For BVI limited partnerships without legal personality formed on or after 1 July 2021, their first “financial period” will commence on its date of formation or registration.

All BVI limited partnerships without legal personality must submit an annual ES report within 18 months from the commencement of the financial period.

Any failure in compliance with BVI economic substance requirements will result in a financial penalty or even the strike-off of the entity. It is advisable that all companies in existence or to be newly incorporated in BVI be fully aware of requirements as well as the submission timeline.

If you need help with incorporating your company in the British Virgin Island, we offer a variety of BVI incorporation packages to fit all your incorporation needs.

Alternatively, if you wish to know if your company falls under the scope of BVI’s economic substance regime? Feel free to get in touch with BBCIncorp and our team will assist you!